ASIC LEI Rules for OTC Derivatives

If your organisation deals in OTC derivatives in Australia, entity identification is no longer a minor back-office detail. Under ASIC’s reporting framework, the data reported for each reportable transaction must include the right entity identifiers, and for eligible entities the Legal Entity Identifier, or LEI, is the preferred code.

That makes the LEI relevant well beyond major banks. Companies, funds, trustees, charities and other legal entities can all be drawn into the reporting process, either as reporting entities or as counterparties whose details must be captured correctly. The current rules allow a short-term fallback when an LEI is not yet available, but the direction is clear: obtain the LEI quickly and use it once issued.

ASIC OTC derivatives reporting rules and LEI basics

ASIC’s Derivative Transaction Rules (Reporting) 2024 require reporting entities to report derivative transaction information for each reportable OTC derivative transaction to a licensed repository or, if none exists, a prescribed repository. That obligation is not limited to trade economics, valuations and timestamps. It also depends on reliable entity data so repositories and regulators can identify who entered the trade, who reported it, and how positions relate across the market.

The LEI fits this job neatly. It is a unique 20-character alphanumeric code based on ISO 17442 and administered through the global LEI system. Each LEI belongs to one legal entity only, and the reference data is published in the Global LEI Index. That public structure matters because it gives market participants a shared source of entity identity rather than a patchwork of internal labels.

In practical terms, the LEI is market infrastructure, not just a reference number.

ASIC 2024 rules on LEI, designated business identifiers and internal IDs

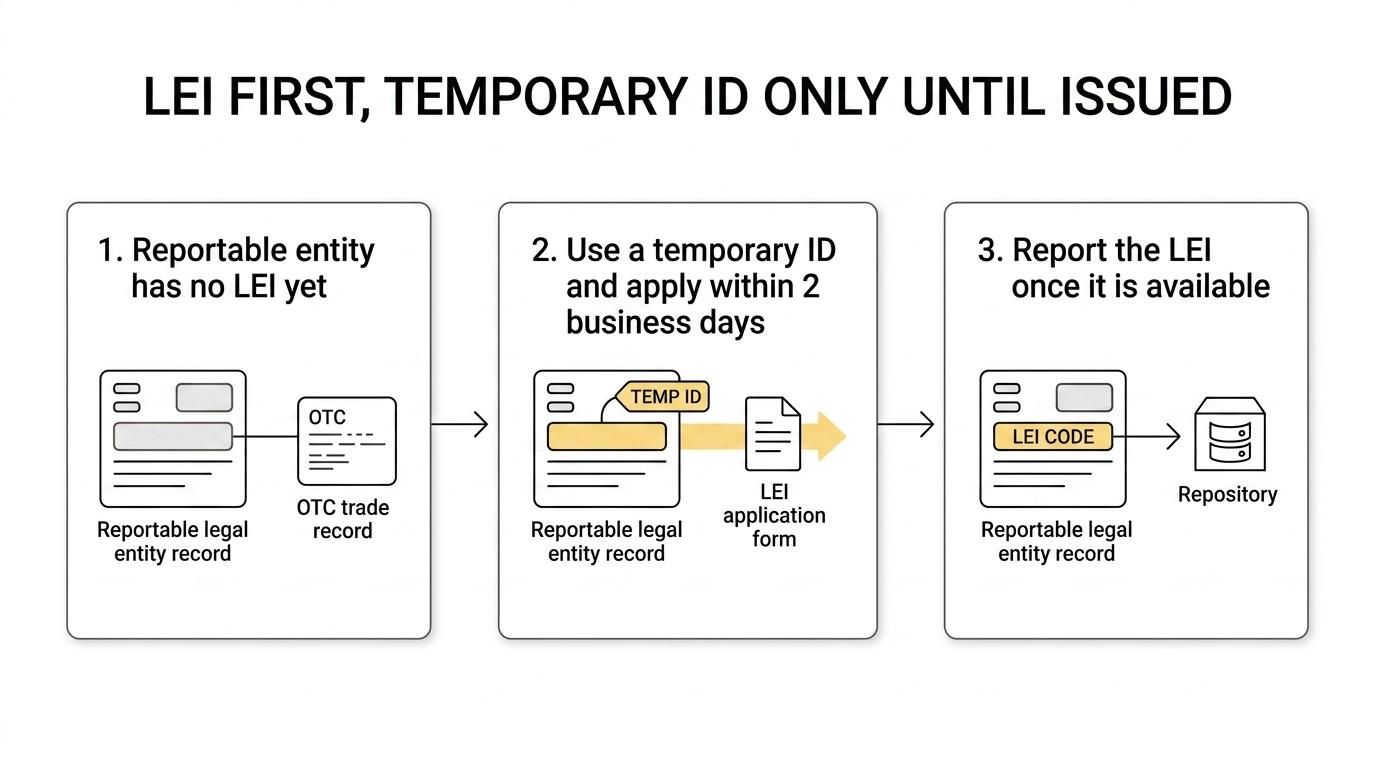

The current ASIC rules are quite direct on the treatment of entity identifiers for reportable OTC derivative transactions. Where an entity is eligible for an LEI and has one, the reporting should use that LEI. This is the cleanest path and the one the rules are built around.

Where an eligible entity does not yet have an LEI, ASIC does allow a temporary substitute. A designated business identifier or an internal entity identifier can be used while the LEI is being obtained. That flexibility is useful, but it comes with a tight timetable. The reporting entity must apply for the LEI within 2 business days after the reporting obligation arises, and must use reasonable endeavours to report the LEI once it becomes available.

That combination tells you a lot about ASIC’s intent. The fallback is there to keep reporting moving, not to provide a long-term alternative to the LEI.

- Eligible entity with an LEI: report the LEI.

- Eligible entity without an LEI yet: use a designated business identifier or internal entity identifier temporarily.

- Application timing: apply for the LEI within 2 business days after the reporting obligation arises.

- After issuance: take reasonable steps to report the LEI once it is available.

For reporting teams, this means the LEI should be treated as part of onboarding and standing data management, not as an item to sort out after a trade has already become reportable.

How ASIC’s current LEI approach differs from the 2013 reporting rules

The present approach is more explicit than the earlier reporting framework. Under the older 2013 rules, ASIC referred to a “standard identifier” for entity counterparties rather than setting out the LEI treatment in the way the 2024 rules now do.

ASIC guidance published in 2018 explained that, from 1 April 2019, financial entities reporting OTC derivative transactions under the 2013 rules had to report a standard identifier for any company or other entity counterparty, excluding individuals. That applied across transactions including CFDs and margin FX. The accepted hierarchy put the LEI first, then AVID if no LEI or interim entity identifier was available, and then BIC if no AVID was available. Even then, ASIC stated its preference that entities obtain an LEI.

The current rules sharpen that preference into a clearer operating model. Rather than relying on a broader standard-identifier hierarchy, the 2024 rules point directly to the LEI for eligible entities and define the temporary fallback path where no LEI is yet available.

| Reporting point | 2013 rules and ASIC guidance | 2024 rules |

|---|---|---|

| Main identifier concept | Standard identifier | Explicit LEI handling |

| Preferred code | LEI preferred, with AVID and then BIC as fallbacks in the older hierarchy | LEI for eligible entities if they have one |

| Short-term substitute | AVID or BIC depending on availability | Designated business identifier or internal entity identifier |

| Action when no LEI exists | ASIC preferred entities obtain one | LEI application required within 2 business days after the reporting obligation arises |

| Direction of travel | LEI encouraged | LEI built into the reporting logic |

This matters for Australian entities still carrying older identifier habits in their systems. If internal processes still assume AVID or BIC will do the job indefinitely, they may now be out of step with the current reporting position.

When temporary entity identifiers are allowed in OTC derivatives reporting

Temporary identifiers can still be useful, especially where a legal entity becomes involved in reportable activity before its LEI has been issued. A recently formed fund, a new special purpose vehicle, or an offshore group entity entering an Australian reporting chain can all create timing pressure.

What matters is the word “temporary”. ASIC’s rules do not present the designated business identifier or internal entity identifier as a standing alternative. The fallback exists only while the LEI is being obtained, and the 2 business day application requirement begins once the reporting obligation arises.

Common situations where the fallback may appear include:

- new fund vehicle

- newly incorporated company

- offshore affiliate entering a reportable structure

- entity moving from AVID or BIC-based processes

- urgent onboarding before first report

If teams wait until after a trade is booked, the timing can become tight very quickly. That is why many market participants now treat LEI readiness as part of pre-trade setup. A live LEI reduces the chance of rushed remediation, mismatched records and repository exceptions.

It also makes communication easier between counterparties, delegates and reporting operations.

Why LEI supports cleaner OTC derivatives reporting data

A local registry number can be useful inside one system or one jurisdiction. OTC derivatives reporting often reaches further than that. Trades may involve international groups, delegated reporting arrangements, global repositories and external counterparties, all of which benefit from a common identity standard.

The LEI gives that common standard. Because it is globally recognised, unique to one entity, and publicly referenceable through the Global LEI Index, it reduces the need for manual mapping between internal identifiers, bank codes and different naming conventions. That can improve data consistency across the trade lifecycle, including amendments, terminations, compressions and transfers.

A current LEI also shows that the entity’s reference data is being maintained rather than left to drift.

There is a strategic benefit here as well. When firms standardise on LEI-based entity data, they are in a better position to support cross-border reporting, internal controls, group-wide data governance and future regulatory change. The gain is not only about meeting one reporting field requirement. It is about using a stable identifier that can travel across systems and obligations with less friction.

Practical LEI steps for Australian companies, funds and charities

The strongest approach is to prepare before the reporting obligation lands. If your organisation may enter reportable OTC derivatives, or may appear in the reporting chain as a legal counterparty, it makes sense to review entity data now. Check whether each relevant entity already has an LEI, whether the code is active, and whether the public reference data matches current registry information.

This review is especially useful for groups with multiple legal vehicles. A corporate group may have one trading entity, one treasury vehicle, one trustee and several fund structures, each with separate legal identity. OTC derivatives reporting depends on the right entity being identified at the right point in the transaction record.

A practical checklist can keep the process focused:

- Map the entities: identify which company, trustee, fund, charity or group vehicle is the legal counterparty to the trade.

- Check LEI status: confirm whether an LEI already exists and whether it is active in the Global LEI Index.

- Apply early: avoid waiting for the first reportable transaction if the entity is likely to need the code.

- Coordinate reporting data: make sure brokers, delegates and internal reporting teams have the correct LEI in standing data.

- Maintain the record: renew on time and keep legal name, address and registry details current.

For organisations with several entities, assisted application and renewal support can reduce internal admin. The same is true where an LEI needs to be transferred from another managing provider, or where reference data maintenance has been neglected and needs to be corrected. Bulk arrangements and ongoing upkeep can make a noticeable difference when reporting obligations sit across a portfolio of funds or group companies.

The current ASIC position is clear enough to act on now. If an entity is eligible for an LEI, the LEI is the key identifier for OTC derivatives reporting, and any fallback is only there to bridge the gap until the code is available. For Australian entities still moving away from older AVID or BIC-based workflows, this is a good time to simplify the identifier stack and treat the LEI as the default code for reportable OTC derivative activity.