When Do You Need an LEI to Trade Derivatives, Bonds, or FX? (Common Scenarios)

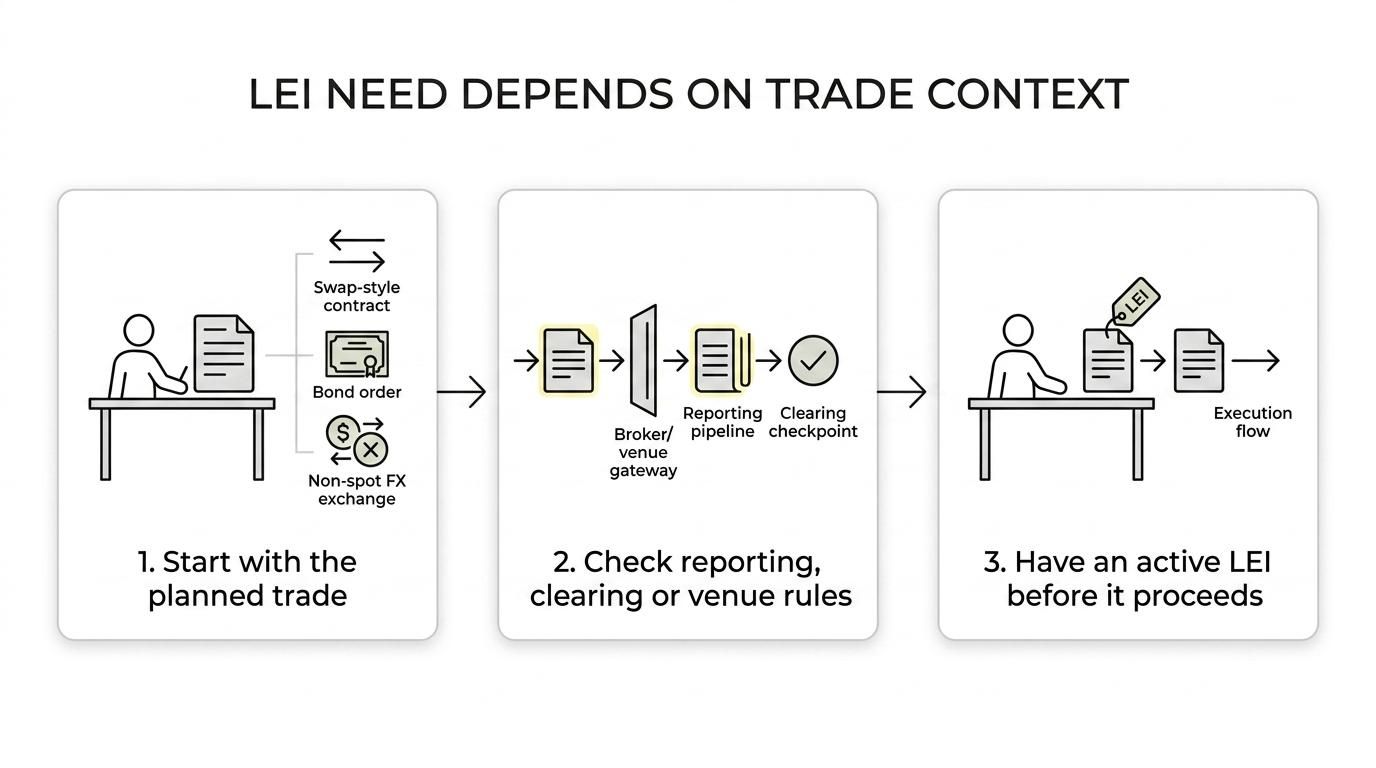

If your organisation trades derivatives, certain bonds, or non-spot FX, the safest starting assumption is simple: you may need an LEI before the trade can be reported, cleared, or even executed.

That is because the Legal Entity Identifier is not just an administrative code. It is the standard identifier regulators, trade repositories, brokers, and venues use to recognise legal entities in financial markets. Once a trade falls inside a reporting regime, the LEI often moves from “useful” to “required”.

What an LEI requirement usually depends on

An LEI is generally required when a transaction must be identified in a regulatory reporting, clearing, or market infrastructure process. The trigger is often not the asset class alone. It is the trading context around that asset class.

In practice, the question is less “Am I trading a bond or an FX contract?” and more “Will this trade be reported, cleared, booked on a regulated venue, or processed through a counterparty that must report me?”

Common triggers include:

- OTC derivatives reporting

- MiFID or MiFIR transaction reporting

- central clearing participation

- execution on a regulated venue

- broker or bank onboarding for institutional trading

- cross-border compliance requirements

A helpful way to think about it is this: if your legal entity needs to appear in a regulator-facing data set, an LEI is often part of the minimum data package.

When an LEI is required for derivatives trading

Derivatives are where LEI requirements are most consistent across major markets.

In the EU, EMIR requires counterparties to derivatives contracts to be identified in trade reports, and LEIs are the standard identifier. In the US, Dodd-Frank swap reporting rules do the same. Similar frameworks exist in Singapore, Hong Kong, Australia, India, and other markets. That means an LEI is commonly required for interest rate swaps, FX forwards, FX swaps, commodity derivatives, equity derivatives, credit derivatives, and many exchange-traded or OTC contracts that sit inside a reporting regime.

This catches more entities than many expect. It is not only banks and major dealers. A corporate hedging interest rates, a fund entering an FX forward, or a treasury vehicle using swaps for risk management may all need an LEI because the transaction itself is reportable.

Here is a simple guide.

| Trading activity | LEI usually needed? | Why |

|---|---|---|

| OTC interest rate swap | Yes | Trade reporting rules typically require legal entity identification |

| FX forward or FX swap | Yes | Non-spot FX is usually treated as a derivative |

| Commodity hedge via OTC derivative | Yes | Reportable derivatives usually need both counterparties identified |

| Exchange-traded futures through an institutional structure | Often yes | Venue, broker, or reporting rules may require it |

| Plain spot FX | Often no | Spot FX is commonly outside derivatives reporting regimes |

| Bond trade on an EU regulated venue | Yes | Transaction reporting rules usually require an LEI |

| OTC bond trade handled by a reporting investment firm | Often yes | The firm may need your LEI to complete reporting |

One detail matters a great deal: a delegated reporting arrangement does not usually remove the need for your entity to have an LEI. If your bank or broker reports on your behalf, it still needs a valid identifier for your entity.

When an LEI is required for bond trading

Bond trading sits in a slightly more nuanced category.

A plain vanilla bond is not automatically subject to the same rules as a derivative. Even so, if the transaction takes place on a regulated venue or is captured by a transaction reporting regime, an LEI can still be mandatory. This has been especially clear in Europe, where MiFID II and MiFIR made LEIs central to transaction reporting across a wide range of financial instruments, including bonds.

That is why many investment firms simply ask for an LEI upfront before allowing an entity to trade bonds. From their side, it is a control issue. If they cannot report the trade correctly, they may not be willing to execute it.

A few common bond-trading situations tend to create LEI requirements:

- trading corporate or sovereign bonds on a regulated market

- using a broker that files transaction reports

- entering repo or securities financing transactions

- clearing bond-related transactions through market infrastructure

Outside Europe, the picture can be less uniform. Some bond markets do not impose an LEI in every case. Still, once institutional reporting, clearing, or cross-border dealing enters the picture, the LEI requirement becomes much more likely.

When an LEI is required for FX trading

FX creates the most confusion because the answer depends heavily on whether the trade is spot or non-spot.

A genuine spot FX transaction, usually settling within two business days, is often outside derivatives reporting frameworks. That means a pure spot trade may not require an LEI in the same way an FX derivative does.

The moment the contract goes beyond spot, the position changes. FX forwards, FX swaps, currency options, and NDFs are generally treated as derivatives. Once that happens, the same reporting logic applies: counterparties often need LEIs.

That distinction is worth keeping in mind:

- Spot FX: Often outside the main derivatives reporting rules

- FX forwards: Usually reportable as derivatives

- FX swaps: Usually reportable as derivatives

- Currency options: Usually reportable as derivatives

- NDFs: Usually reportable as derivatives

For Australian corporates, this is especially relevant in treasury activity. A business might assume it is “just managing currency exposure”, yet the instrument chosen by the bank or dealer may be a forward or swap. If it is reportable, the LEI requirement can appear very quickly.

The Australian position on LEIs for trading

Australia is not outside this global pattern. ASIC’s derivative transaction reporting framework has moved in line with international standards, and LEIs are part of that structure for reportable OTC derivatives.

That means Australian entities dealing in reportable OTC derivatives should take LEI readiness seriously, even when the counterparty is doing much of the reporting work. If the trade must be reported with standard identifiers, waiting until trade date to organise an LEI can slow things down.

This matters for entities that may not think of themselves as “financial market participants” in the traditional sense. A company hedging rates, a fund manager entering currency contracts, or a charity with an investment structure can still be caught if the instrument and reporting context fit the rules.

A practical point often gets missed here. The LEI is not only about legal compliance in theory. It is also about operational acceptance. Dealers, custodians, platforms, and reporting teams prefer to have the LEI in place well before a transaction is booked.

Thresholds, exemptions, and why small size does not always save you

Many entities ask whether there is a minimum trade size before an LEI is needed. Often, the answer is no.

Thresholds do matter in some frameworks, but they usually affect classification, clearing obligations, or reporting responsibility, not whether the entity identifier is needed once a reportable trade exists. A non-financial counterparty below a clearing threshold may still need an LEI if its trade is being reported by a financial counterparty.

That is why small or occasional users of derivatives should be careful about relying on “we are below threshold” as a complete answer.

A few points help cut through the confusion:

- Clearing threshold: May affect whether your entity must clear certain derivatives

- Reporting trigger: May still apply even when clearing does not

- Delegated reporting: Usually still requires your LEI

- Trade size: Does not automatically remove the identifier requirement

There are some exceptions. Spot FX is the big one. Some intra-group arrangements may also fall under specific exemptions in certain jurisdictions. Individuals are another special case because natural persons do not obtain LEIs in the same way legal entities do.

Still, for companies, trusts, funds, partnerships, and other legal structures active in institutional markets, the safer view is that any reportable trade may need a live LEI.

Common scenarios where an LEI is needed before trading

It helps to move from rules to real-life situations.

An Australian company enters an FX forward to hedge US dollar invoices. Even if it only does this a few times a year, the contract is generally a derivative, not spot FX. The bank may need the company’s LEI before the trade can be processed inside its reporting framework.

A wholesale fund buys bonds through an EU-connected broker. Even though the product is “just a bond”, the broker may be subject to transaction reporting requirements and may refuse to trade until the fund’s LEI is active.

A corporate treasury team uses an interest rate swap tied to debt financing. The swap is reportable. If the entity has no LEI, onboarding and execution may stall while the identifier is obtained.

A group treasury centre executes transactions for related entities across borders. One intra-group assumption can create delays if one affiliate actually needs to be separately identified for reporting or venue access.

These scenarios tend to share the same pattern:

- A legal entity is trading, not an individual

- The trade is reportable, clearable, or venue-based

- The bank, broker, or platform needs a standard counterparty identifier

- The LEI is expected before execution or reporting cut-off

Why firms often ask for an LEI even before the law is discussed

Market practice can be stricter than the bare minimum in regulation.

A broker or bank may ask for an LEI during onboarding because it wants a single, reliable entity identifier across KYC, settlement, reporting, and reconciliation. That reduces name-matching errors and makes lifecycle events easier to manage. If the entity later trades derivatives, bonds, or financing transactions, the identifier is already in place.

This is one reason many entities first hear about LEIs from their counterparty rather than directly from a regulator. The operational side of the market has already built the LEI into core workflows.

For active trading organisations, having an active LEI can support:

- cleaner onboarding with brokers and banks

- more reliable trade reporting data

- smoother cross-border trading access

- simpler renewals of existing market relationships

What to do before your next derivative, bond, or FX trade

If your entity expects to trade anything beyond simple spot FX, it is sensible to check LEI status early.

First, confirm whether the product is a derivative, a reportable bond transaction, or a trade executed through a reporting investment firm. Next, ask the broker, dealer, or platform whether they require an active LEI before execution. Then check whether your entity already has one, and whether it is active rather than lapsed.

Where a new LEI or renewal is needed, speed matters. A service that handles the application and data maintenance on the client’s behalf can save time, especially if a trade is pending. LEI Service Australia, for example, offers new registrations, renewals, transfers, multi-year plans, free reference data updates, and same-day issuance for orders placed before 6 pm, with English-speaking support by phone and email.

A short pre-trade checklist can prevent last-minute delays:

- confirm the exact instrument type

- ask who is responsible for reporting

- verify whether your entity’s LEI is active

- renew before expiry if needed

- make sure legal entity details match registry records

- allow time if the trade is imminent

In many cases, the answer to “when do you need an LEI to trade?” is earlier than expected. Not after the trade is agreed. Not when a report is rejected. Usually before the trade can move ahead with confidence.